Health Insurance 101 for Black Adults: How to Choose the Right Plan and Avoid Costly Mistakes

Summary

Health insurance helps protect you from high medical costs and gives you access to care when you need it. You can get coverage through your job, government programs like Medicaid or Medicare, or the Health Insurance Marketplace.

Key things to know:

Black adults are more likely to face barriers to affordable and quality healthcare.

Choosing the wrong plan can lead to unexpected bills and limited access to care.

Always check your premium, deductible, and network before enrolling.

Staying in-network and understanding your coverage saves money.

At BHE Foundation, we believe understanding your health insurance is a key step toward health equity, empowerment, and informed decision-making.

Why Health Insurance Matters—Especially for Our Community

Health insurance isn’t just paperwork - it can directly impact your ability to get care, manage chronic conditions, and protect your finances.

In the U.S., Black communities continue to face systemic barriers to quality healthcare:

Black adults are more than twice as likely to experience poverty compared to white adults.

The median income for Black households is significantly lower, impacting access to employer-sponsored insurance.

About 18% of Black adults report experiencing discrimination in healthcare settings, compared to just 3% of white adults.

A recent national analysis found Black Americans experience worse health outcomes on nearly 70% of measured health indicators.

Even when insured, cost barriers, lack of understanding, and system complexity can prevent people from actually using their benefits. Health literacy is health equity. Understanding your insurance is a key step toward advocating for yourself, accessing care, and avoiding unnecessary financial stress. This is where health literacy becomes power.

Health literacy is health equity!

So, What Is Health Insurance?

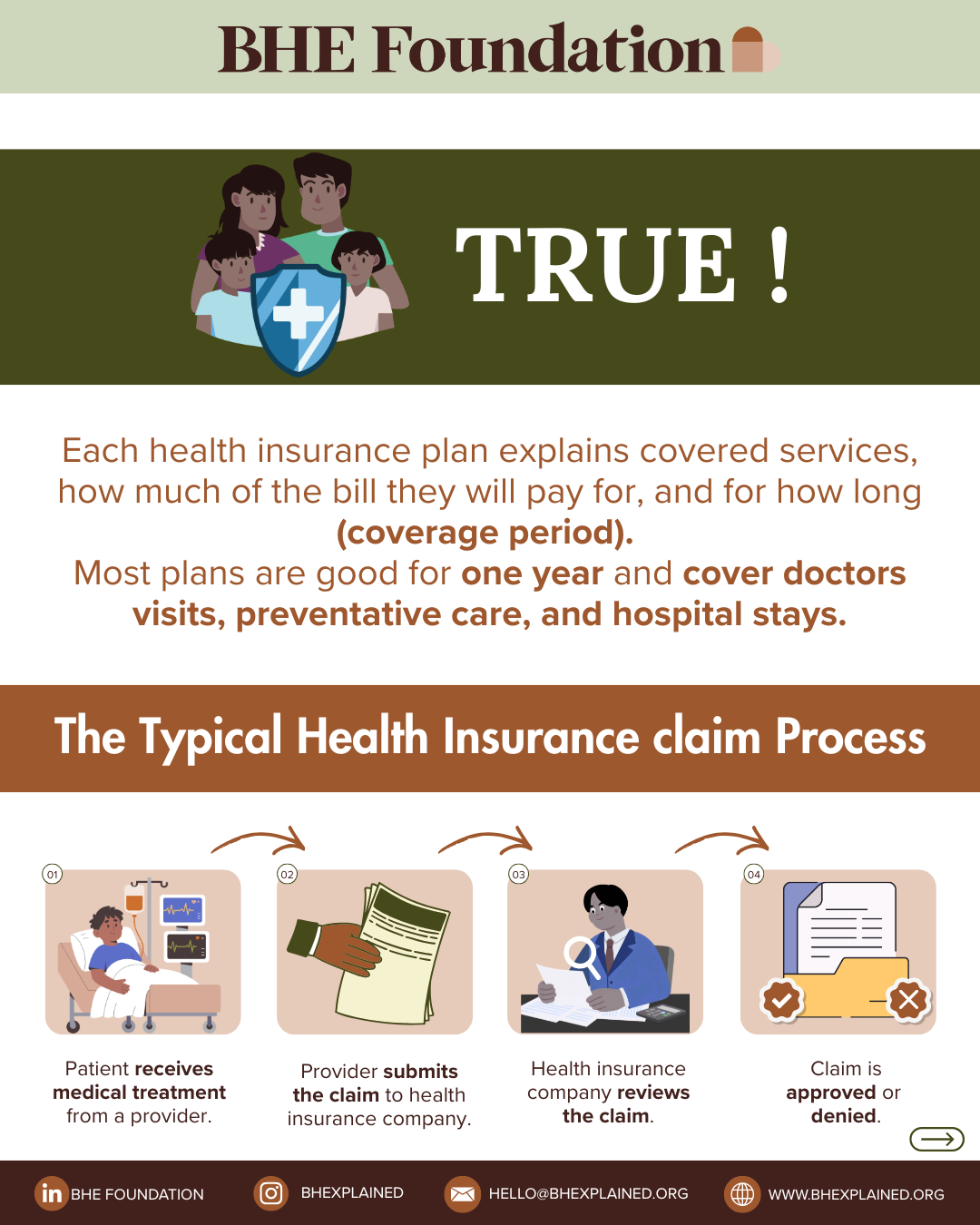

Health Insurance is a contract where a health insurance company pays for or reimburses your health care costs. This can be between you and an insurance provider or with your employer. A health insurance plan describes the health care items and services that the insurance company will help pay for (covered services), how much it will pay, and for how long. Most health insurance plans last for a year at a time.

Health insurance is a contract between you and an insurance provider that helps pay for medical services like:

Doctor visits

Prescriptions

Preventive care

Hospital stays

Health plans are often bundled with vision and dental plans but can be purchased separately.

Types of Health Insurance

There are two types of health insurance: Public and Private. Public health insurance is provided through the government, such as Medicare and Medicaid. Private health can be through an employer, the Health Insurance Market or purchased directly from the insurance provider.

Public Insurance

Medicaid – For individuals and families with limited income

Medicare – Typically for adults 65+ or with certain disabilities

TRICARE

VA Coverage

Black Americans are twice as likely to rely on Medicaid, making it a critical access point for care.

Private Insurance

Employer-sponsored plans

Marketplace (Affordable Care Act plans)

Individual plans purchased directly from insurance provider

When Can You Enroll?

Most people enroll during Open Enrollment. This is the yearly period from November 1 to January 30 during which you can buy health insurance through the Marketplace or make changes to your existing health plan. Some employers may have different open enrollment dates and the specific timeframe depends on various factors. You should check with your employer or insurance provider to confirm your open enrollment period. Here we will cover the process of choosing the right insurance plan for you.

You may also qualify for a Special Enrollment Period, outside of open enrollment, if you experience a life change such as:

Turning 26 (aging out of a parent’s plan)

Job loss or change in employment

Moving to a new state

Marriage, divorce, or having a child

How to Choose the Right Plan

Choosing the right health insurance plan is a big decision. Though there is no “perfect plan,” you should choose a plan that best fits your needs, family, and lifestyle/budget. Making an informed decision now can save you money and stress later. Here are some things to consider when you make your decision:

Ask yourself:

Do I want to keep my current doctor? (Are they in-network?)

Do I take medications regularly—and are they covered?

Do I expect any major health needs this year?

Can I afford the monthly premium and out-of-pocket costs?

Understanding the Costs (What You’re Really Paying)

Your health insurance plan will include the following costs:

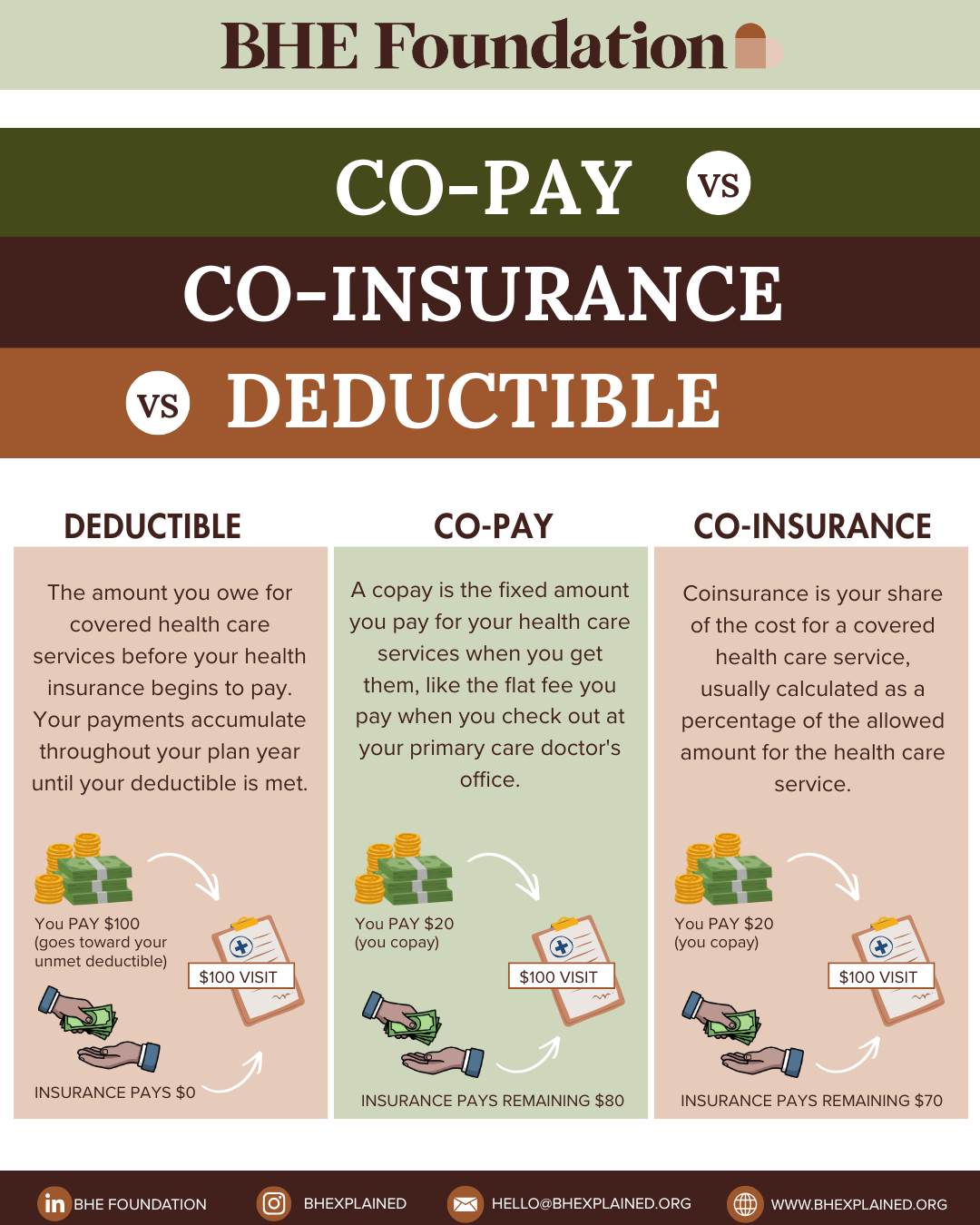

Premium - Your monthly payment to have insurance (like a subscription).

Deductible - The amount a person must pay for covered health services received before their insurance plan begins to pay. Don’t worry, some covered services will be paid for without having to meet your deductible. Covered preventative care services, such as physicals and pap smears, are typically paid 100% by your insurance plan without meeting the deductible.

Copayment (Copay) - A fixed cost for services (e.g., $25 for a doctor visit).

Coinsurance - A percentage you pay after meeting your deductible (e.g., 20% of a bill).

Out-of-Pocket Maximum - The most you’ll pay in a year. This usually includes deductibles, copays, and coinsurance. Once you hit this, your insurance will pay 100% of future covered services for the rest of the year (coverage period).

Let’s see how this works

Let’s say you need a surgery that costs $15,000.

Your annual deductible is $500

You’ve already paid $250 toward your deductible this year

At the time of your surgery, you will need to pay the remaining $250 to meet your deductible.

Once your deductible is met, your insurance begins to share the cost.

For example:

If your plan has 20% coinsurance, your insurance will cover 80% of the remaining cost, and you will be responsible for 20%.

Remaining balance after deductible: $14,750

Your 20% coinsurance: $2,950

Insurance pays: $11,800

Total You Pay:

$250 (remaining deductible)

$2,950 (coinsurance)

= $3,200 total out-of-pocket

Why This Matters

Even with insurance, large medical expenses can add up quickly. Understanding your deductible and coinsurance helps you plan ahead and avoid unexpected bills.

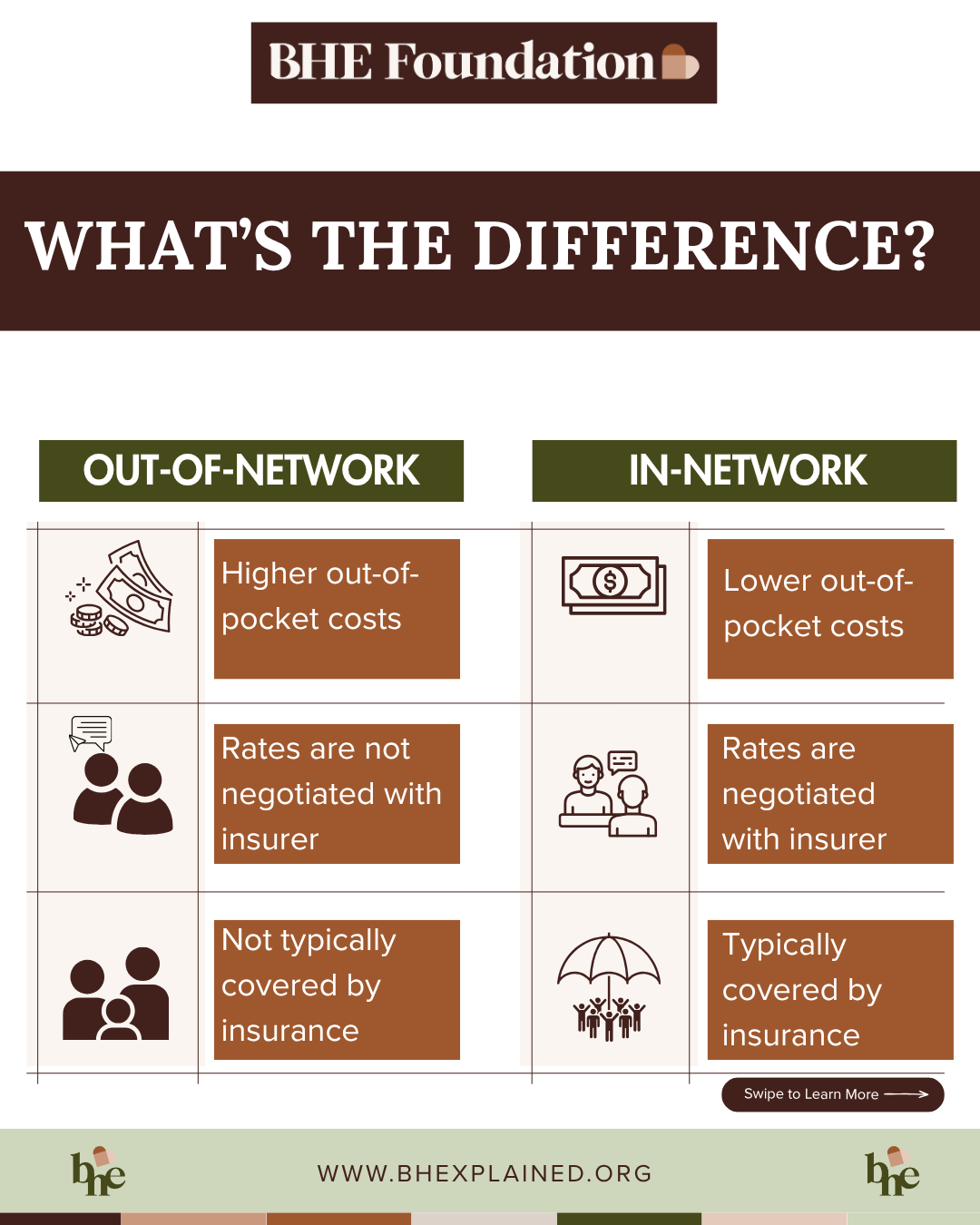

In-Network vs. Out-of-Network (Where You Go Matters)

In a health insurance plan description, you will see the terms in-network and out-of-network. These terms distinguish the cost of the service or item provided and how much the health insurance (noted as a percentage) will pay. In-network providers have a negotiated rate with the insurance plan to provide services or items to consumers enrolled in the plan. Whereas an out-of-network provider does not have a negotiated rate.

In-network providers have agreements with your insurance → lower cost

Out-of-network providers do not → higher cost

Bottom line: Staying in-network can significantly reduce your expenses.

Pre-Existing Conditions (What You Should Know)

Under current law, insurance companies cannot deny coverage or charge more based on pre-existing conditions.

However, always confirm:

Coverage details

Medication access

Specialist availability

What Is Prior Authorization?

Some services require approval before you receive care. Prior Authorizations is when health providers get approval from your health insurance before you can have a certain service or prescription. Also known as preauthorization and prior approval, prior authorization can be necessary for non-emergency surgeries and expensive prescriptions.

When your provider submits a request, they explain why the service or prescription is needed and may include previous things that were tried to address the health issue. Review of the request can take up to 30 days, but once a decision is made, you and your provider will be notified in writing. Prior authorizations are only approved for a specific period of time.

Important: Without approval, your insurance may not cover the service.

Why This Matters for You

Too often, people choose health insurance without fully understanding it, and end up:

Avoiding care due to cost

Receiving unexpected bills

Missing preventive services

Understanding your health insurance is more than paperwork—it’s power.

When you understand your health insurance, you can:

Advocate for yourself in healthcare settings

Make informed financial decisions

Access care earlier and more consistently

Protect your long-term health

When you know how your plan works, you can:

Access care with confidence

Avoid unexpected medical bills

Advocate for your health

Make informed decisions for yourself and your family

Health insurance is more than a requirement; it’s a tool. A tool that, when understood, can help close gaps in care, reduce disparities, and improve outcomes in our communities.

Health literacy is health equity—and it starts with understanding your coverage. At BHE Foundation, our goal is to make health information clear, accessible, and relevant—so you can take control of your health journey.

Here’s some resources for you as you take control of your health journey:

Healthcare.gov - federal website to check eligibility, compare plans, and find basics on the Affordable Care Act (ACA).

DC Health Link- The District of Columbia’s health insurance exchange marketplace website to compare, shop, and enroll in health plans.

Maryland Health Connection - Maryland’s health insurance exchange marketplace website to compare, shop, and apply for financial help for health plans.

Ohio Department of Insurance: Health - The Ohio Department of Insurance site to get information and help on choosing health plans.

Virginia’s Insurance Marketplace- Virginia’s health insurance exchange marketplace website to compare, shop, and enroll in health plans.

About the Author: Christine Anyanwu, MPH

Christine Anyanwu is from Baltimore, MD. She earned a Bachelor of Science in Chemistry from Towson University and a Master of Public Health with a concentration in Community and Population Health from the University of Maryland, Baltimore. She is passionate about health equity and social drivers of health. Her professional background includes academic research and program evaluation in the injury and violence prevention field. She enjoys watching sporting events (particularly Baltimore Ravens and Boston Celtics games), collecting comics, and finding new restaurants.

About the Author: Ake’lah Chambers

Ake’Lah Chambers is a healthcare consultant and founder of IntegrityWorks Solutions, bringing over a decade of experience in policy development, regulatory compliance, and program management. Known for strategic insight and strengthening organizational systems, she helps providers improve operations, care delivery, and alignment with state and federal standards. Ake’Lah holds a Bachelor of Science in Health Administration from Norfolk State University and began her career supporting assisted living and behavioral health providers. Her leadership experience includes serving as Director of Human Resources at a dual-diagnosis facility, where she significantly reduced staff turnover, implemented mentorship initiatives, and contributed to measurable revenue growth. Beyond consulting, Ake’Lah champions access and inclusion in healthcare and disability communities. She founded AccessAble Events to create inclusive social experiences for adults with intellectual and developmental disabilities and leads networking events to strengthen industry collaboration. She is actively involved in community leadership and professional organizations throughout Hampton Roads, where she continues to champion equity, collaboration, and sustainable healthcare solutions.